Bibliometric Analysis Research on Audit Nexus in Corporate Governance

Abstract

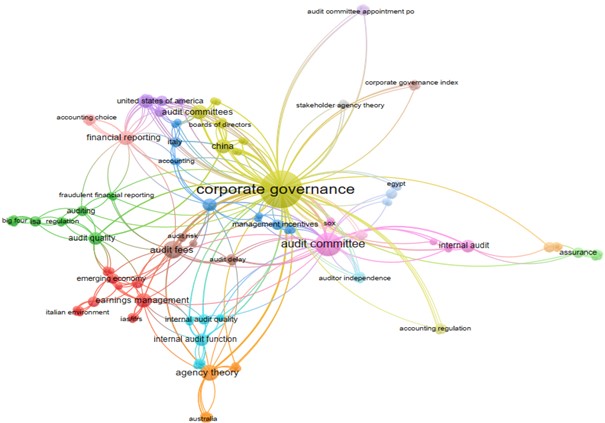

Audit study on corporate governance and its influence on the corporate organisation is expanding exponentially. It has been undeniable after the 2007-2008 financial crisis and corporate scandals. This review provides an overview of the evolution of scholarly literature on the relationship between audit and corporate governance in peer-reviewed publications published between 2010 and 2020. The study has used a bibliometric technique to review 48 researched documents from the Scopus database. The review highlights document type, publication trend, journal types, influential authors, impactful papers, and keyword co-occurrence network through VOSviewer visualisation. In addition, the findings uncover new trends that have surfaced over the past few decades and suggest possible future lines of research. This study contributes to our understanding of audit in corporate governance studies by reviewing documents systematically using bibliometric techniques and VOSviewer analysis for the study period.

References

Akbar, S., Kharabsheh, B., Poletti-Hughes, J., & Shah, S. Z. (2017). Board structure and corporate risk-taking in the UK financial sector. International Review of Financial Analysis, 50(March), 101-110. https://doi.org/10.1016/j.irfa.2017.02.001

Al-Matari, E., & Mgammal, M. (2019). The moderating effect of internal audit on the relationship between corporate governance mechanisms and corporate performance among Saudi Arabia listed companies. Contaduria y Administracion, 64(4), 1-27. https://doi.org/10.22201/fca.24488410e.2020.2316

Al-Najjar, B., & Abed, S. (2014). The association between disclosure of forward-looking information and corporate governance mechanisms: Evidence from the UK before the financial crisis period. Managerial Auditing Journa, 29(7), 578-595. https://doi.org/10.1108/MAJ-01-2014-0986

Al-Najjr, B., & Abed, S. (2015). The association between disclosure of forward-looking information and corporate governance mechanisms: Evidence from the UK before the financial crisis period. Managerial Auditing Journal, 29(7), 578-595. https://doi.org/10.1108/MAJ-01-2014-0986

Alander, E. . (2019). Clash of corporate governance logics obscuring auditor independence. International Journal of Auditing, 32(2), 336-351. https://doi.org/10.1111/ijau.12164

Ali, A., Ahmi, A., & Ahmad, W. N. (2018). The Current State of the Internal Audit Research: A Bibliometric Analysis. 5th International Conference on Accounting Studies (ICAS 2018) 16-17 October 2018, Penang, Malaysia.

Almqvist, R. G., Grossi, J., van Helden, C., & Reichard. (2013). Editorial. Public Sector Governance and Accountability. Critical Perspectives on Accounting, 24, 479-487. https://doi.org/10.1016/j.cpa.2012.11.005

AlQadasi, A., & Abidin, S. (2018). The effectiveness of internal corporate governance and audit quality: the role of ownership concentration - Malaysian evidence. Corporate Goverannce, 18(2), 233-253. https://doi.org/10.1108/CG-02-2017-0043

Alzeban, A. (2015). Influence of audit committees on internal audit conformance with internal audit standards. Managerial Auditing Journa, 30(6/7), 539-559. https://doi.org/10.1108/MAJ-12-2014-1132

Alzeban, A. (2018). CEO involvement in selecting CAE, internal audit competency and independence, and financial reporting quality. Journal of Business Economics and Management, 19(3), 456-473. https://doi.org/10.3846/jbem.2018.6264

Balancieri, R. (2004). Análise de redes de pesquisa em uma plataforma de gestão em ciência e tecnologia: uma aplicação à Plataforma Lattes. Universidade Federal de Santa Catarina,.

Barth, M., Haustein, S., & Scheidt, B. (2014). The life sciences in German-Chinese cooperation: an institutional-level co-publication analysis. Scientometrics, 98(1), 99-117. https://doi.org/10.1007/s11192-013-1147-9

Behrend, J., & Eulerich, M. (2019). Four Decades of Audit Committee Research: A Bibliometric Analysis (1977-2018). Retrived 13/03/2020, 43. https://doi.org/Behrend, Joel and Eulerich, Marc, Four Decades of Audit Committee Research: A Bibliometric Analysis (1977-2018) (November 30, 2019). https://doi.org/10.2139/ssrn.3496040

Benckendorff, P., & Zehrer, A. (2013). A network analysis of tourism research. Annals of Tourism Research, 43, 121-149. https://doi.org/10.1016/j.annals.2013.04.005

Bhattacharya, A., & Banerjee, P. (2020). An empirical analysis of audit pricing and auditor selection: evidence from India. Managerial Auditing Journa, 35(1), 111-151. https://doi.org/10.1108/MAJ-11-2018-2101

Borokhovich, K. A., Bricker, R. J., Brunarski, K. R., & Simkins, B. J. (1995). Finance Research Productivity and Influence. Journal of Finance, 50(5), 1691-717. https://doi.org/10.1111/j.1540-6261.1995.tb05193.x

Brown, J., Popova, O., & Velina, K. (2016). The Interplay of Client Management and the Audit Committee on Auditor Performance. Current Issues in Auditing, 10(1), 11-17. https://doi.org/10.2308/ciia-51424

Castriotta, M., Loi, M., Marku, E., & Naitana, L. (2019). What's in a name? Exploring the 794 conceptual structure of emerging organizations. Scientometrics, 118(2), 407-437. https://doi.org/10.1007/s11192-018-2977-2

Chung, H. H., & Wynn, J. P. (2014). Corporate governance, directors'' and officers' insurance premiums and audit fees. Managerial Auditing Journa, 29(2), 173-195. https://doi.org/10.1108/MAJ-04-2013-0856

Comerio, N., & Strozzi, F. (2019). Tourism and its economic impact: A literature review using bibliometric tools. Tourism Economic, 25(1), 109-131. https://doi.org/10.1177/1354816618793762

Crawford, M., & Stein, W. (2002). Auditing Risk Management: Fine in Theory but who can do it in Practice? International Journal of Auditing, 6, 119-131. https://doi.org/10.1111/j.1099-1123.2002.tb00009.x

Cunha, P. ., Toigo, L., & Picoli, M. . (2016). Scientific production on the Audit Committee: A Bioblimtric and Sociometric Analysis of International Journals. Digital Library of Journals, 8(1), 26-46. https://doi.org/10.5380/rcc.v8i1.35902

Dabi'c, M., Maley, J., Dana, L. P., Novak, I., Pellegrini, M. M., & Caputo, A. (2019). Pathways of SME internationalization: A bibliometric and systematic review. Small Business Economics, 55, 705-725. https://doi.org/10.1007/s11187-019-00181-6

Ellegaard, O., & Wallin, J. (2015). The bibliometric analysis of scholarly production: How great is the impact? Scientometrics, 105, 1809-1831. https://doi.org/10.1007/s11192-015-1645-z

Ellwood, S., & Garcia-Lacalle, J. (2015). Examining Audit Committees in the Corporate Governance of Public Bodies. Public Management Review, 18(8), 1138-1162. https://doi.org/10.1080/14719037.2015.1088566

Fachriza, Z., & Mardijuwono, A. (2020). Corporate Governance, Ownership Concentration and Audit Quality. Cuadernos de Economia, 43(122), 105-242.

Falagas, M., Pitsouni, E., Malietzis, G., & Pappas, G. (2008). Comparison of PubMed, Scopus, Web of Science, and Google Scholar: strengths and weaknesses. The FASEB Journal, 22(2), 338-342. https://doi.org/10.1096/fj.07-9492LSF

Gaoa, L., & Kling, G. (2012). The impact of corporate governance and external audit on compliance to mandatory disclosure requirements in China. Journal of International Accounting, Auditing and Taxation, 21(1), 17-31. https://doi.org/10.1016/j.intaccaudtax.2012.01.002

Gebrayel, E., Jarrar, H., Salloum, C., & Lefebvre, Q. (2018). Effective association between audit committees and the internal audit function and its impact financial reporting quality: Empirical evidence from Omani listed firms. International Journal of Auditing, 22(2), 197-213. https://doi.org/10.1111/ijau.12113

Gramling, A., & Hermanson, D. (2009). Assisting the Audit Committee during financial crisis. Corporate Governance and Internal Auditing, 24(3), 41-44.

Gupta, P., & Sharma, A. M. (2014). A study of the impact of corporate governance practices on firm performance in Indian and South Korean companies. Procedia - Social and Behavioral Sciences, 133, 4-11. https://doi.org/10.1016/j.sbspro.2014.04.163

Harjoto, M., Laksmana, I., & Lee, R. (2015). The impact of demographic characteristics of CEOs and directors on audit fees and audit delay. Managerial Auditing Journa, 30(8/9), 963-997. https://doi.org/10.1108/MAJ-01-2015-1147

Hirsch, J. (2005). An Index to quantify an Individual's scientific research output. Proceedings of the National Academy of Sciences of the United States of America, 102(46), 16569-16572. https://doi.org/10.1073/pnas.0507655102

Hopt, K. J. (2002). Modern company and capital market problems: Improving European corporate governance after Enron. Journal of Corporate Law Studies, 3(2), 221-268. https://doi.org/10.1080/14735970.2003.11419902

Houge, M., Ahmed, K., & va Ziji, T. (2017). Audit Quality, Earnings Management, and Cost of Equity Capital: Evidence from India. International Journal of Auditing, 21(2), 177-189. https://doi.org/10.1111/ijau.12087

IFAC. (2014). International Framework: Good Governance in the Public Sector.

Janssen, M. A. (2007). An update on the scholarly networks on resilience, vulnerability, and adaptation within the human dimensions of global environmental change. Ecology and Society, 12(2), 1-18. https://doi.org/10.5751/ES-02099-120209

Johl, S., Johl, S., Subramaniam, N., & Cooper, B. (2013). Internal audit function, board quality and financial reporting quality: Evidence from Malaysia. Managerial Auditing Journa, 28(9), 1-38. https://doi.org/10.1108/MAJ-06-2013-0886

Knechel, W., Niemi, L., & Sundgren, S. (2008). Determinants of auditor choice: evidence from a small client market. International Journal of Auditing, 12(1), 65-88. https://doi.org/10.1111/j.1099-1123.2008.00370.x

Kooli, C. (2019). Governing and managing higher education institutions: The quality audit contributions. Evaluation and Program Planning, 77(101713), 1-9. https://doi.org/10.1016/j.evalprogplan.2019.101713

Kooli, C., & Abadli, R. (2021). Could Education Quality Audit Enhance Human Resources Management Processes of the Higher Education Institutions? Vision, 1-9. https://doi.org/10.1177/09722629211005599

Kooli, C., Jamrah, A., & Al-Abri, N. (2019). Learning from Quality Audit in Higher Education Institutions: A Tool for Community Engagement Enhancement. FIIB Business Review, 8(3), 218-228. https://doi.org/10.1177/2319714519863559

Macias-Chapula, C. A. (1998). O papel da informetria e da cienciometria e sua perspectiva nacional e internacional. Revista Ciência Da Informação, 27(2), 134-140. https://doi.org/10.1590/S0100-19651998000200005

Madani, F., & Weber, C. (2016). The evolution of patent mining: Applying bibliometrics analysis and keyword network analysi. World Patent Information, 46, 32-48. https://doi.org/10.1016/j.wpi.2016.05.008

Matonti, G., Tucker, J., & Tommasetti, A. (2016). Auditor choice in Italian non-listed firms. Managerial Auditing Journal, 31(4/5), 458-491. https://doi.org/10.1108/MAJ-07-2015-1215

Merigo, J. M., Gil-Lafuente, A. M., & Yager, R. R. (2015). An Overview of Fuzzy Research with Bibliometric Indicators. Applied Soft Computing, 27, 420-433. https://doi.org/10.1016/j.asoc.2014.10.035

Mustafa, S., & Ben Youssef, N. (2010). Audit committee financial expertise and misappropriation of assets. Managerial Auditing Journa, 25(3), 208-225. https://doi.org/10.1108/02686901011026323

Nerur, S. P., Rasheed, A. A., & Natarajan, V. (2007). The intellectual structure of the strategic management field: An author co-citation analysis. Strategic Management Journa, 29(3), 319-336. https://doi.org/10.1002/smj.659

O'Leary, C., Boolaky, P., & Delameu, D. (2013). Accounting regulation changes: Differing attitudes of directors and auditors. International Journal of Accounting Auditing and Performance EValuation, 9(4), 365-387. https://doi.org/10.1504/IJAAPE.2013.057523

Qeshtaa, M., & Ali, B. (2020). The moderating effect of the effectiveness of the audit committee between ownership concentration and intellectual capital disclosures among companies in gulf co-operation council. International Journal of Psychosocial Rehabilitation, 24(1), 5979-5986.

Samaha, K., Khlif, H., & Hussainey, K. (2015). The impact of board and audit committee characteristics on voluntary disclosure: A meta-analysis. Journal of International Accounting, Auditing and Taxation, 24, 13-28. https://doi.org/10.1016/j.intaccaudtax.2014.11.001

Sarens, G., & Abdolmohammadi, M. (2011). Monitoring effects of the internal audit function: Agency theory versus other explanatory variables. Internatioanl Journal of Auditing, 15(1), 1-20. https://doi.org/10.1111/j.1099-1123.2010.00419.x

Sarens, G., & De Beelde, I. (2006). The relationship between internal audit and senior management. International Journal of Auditing, 10(3), 219-241. https://doi.org/10.1111/j.1099-1123.2006.00351.x

Saunders, M., Lewis, P., & Thornhill, A. (2009). Research Methods for Business Students (5th ed.). Prentice Hall.

Seuring, S., Müller, M., Westhaus, M., & Morana, R. (2005). Conducting a literature review-The example of sustainability in supply chains. Research Methodologies in Supply Chain Management: In Collaboration with Magnus Westhaus, 91-106. https://doi.org/10.1007/3-7908-1636-1_7

Shan, Y. G. (2014). The impact of internal governance mechanisms on audit quality: A study of large listed companies in China. International Journal of Accounting, Auditing and Performance Evaluation, 10(1), 68-90. https://doi.org/10.1504/IJAAPE.2014.059183

Sinnakkannu, J., & Nassir, A. M. (2008). Revisiting the causes of the east Asian Financial Crisis: Was it predictable? International Journal of Economic Perspectives, 2(2), 78-93.

Soltani, B. (2014). The anatomy of corporate fraud: a comparative analysis of high profile American and European corporate scandals. Journal of Business Ethics, 120(2), 251-274. https://doi.org/10.1007/s10551-013-1660-z

Souza, F. C., Rover, S., Gallon, A. V., & Ensslin, S. R. (2008). Analise das IES da Área de Ciências Contábeis e de seus Pesquisadores por meio de sua Produção Cientifica. Revista Contabilidade Vista & Revista, 19(3), 15-38.

Srivastava, V., Das, N., & Pattanayak, J. (2019). Impact of corporate governance attributes on cost of equity: Evidence from an emerging economy. Managerial Auditing Journa, 34(2), 142-161. https://doi.org/10.1108/MAJ-01-2018-1770

Tunger, D., & Eulerich, M. (2018). Bibliometric analysis of corporate governance research in German-speaking countries: applying bibliometrics to business research using a custom-made database. Scientometrics, 117(3), 2041-2059. https://doi.org/10.1007/s11192-018-2919-z

Vadasi, C., Bekiaris, M., & Andrikopoulo, A. (2020). Corporate governance and internal audit: an institutional theory perspective. Corporate Governance, 20(1), 175-190. https://doi.org/10.1108/CG-07-2019-0215

Van Eck, N., & Waltman, L. (2014). N. In Ding, R. Rousseau, & D. Wolfram (Eds.), Measuring scholarly impact. Methods and practice(pp. 285-320). Springer International Publishing. https://doi.org/10.1007/978-3-319-10377-8_13

Vieira, E., & Gomes, J. A. (2009). A comparison of Scopus and Web of Science for a typical university. Scientometrics, 87(587), 1-25. https://doi.org/10.1007/s11192-009-2178-0

Wallin, J. (2005). Bibliometric Methods: Pitfalls and Possibilities. Basic and Clinical Pharmacology & Toxocology, 97(5), 261-275. https://doi.org/10.1111/j.1742-7843.2005.pto_139.x

This work is licensed under a Creative Commons Attribution 4.0 International License.

Copyright for this article is retained by the author(s), with first publication rights granted to the journal.

This is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).