Determinants of Tax Revenue in Sierra Leone: Application of the ARDL Framework

Abstract

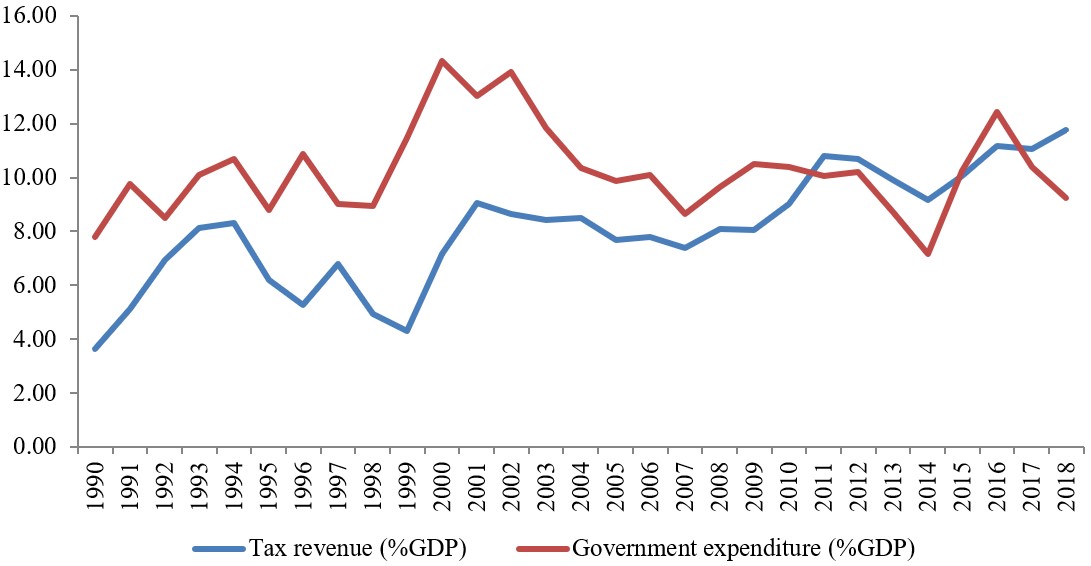

The aim of this paper is to investigate the determinants of tax revenue in Sierra Leone, over the period 1990Q1 to 2020Q1, within the context of the ARDL estimation procedure. The result from the ARDL Bound test for cointegration suggests that a long-run relationship exists among the variables. The long run analysis indicates that real GDP (Y), openness (Op) and official development assistance (ODA) are the main determinants of tax revenue (TR) in Sierra Leone, with positive coefficients. This result is in tandem with the short run findings, which establishes a positive relationship between tax revenue and its regressors- real GDP and openness. However, the short run result also suggests that inflation has a negative impact on tax revenue. The findings confirm that any short-run disequilibrium to the long-run can be corrected at the 11 percent speed of adjustment quarterly, albeit at a low speed of adjustment. The diagnostic result shows that approximately 75 percent of the variation in the dependent variable is explained by the regressors based on the value of the R-squared. It also confirms that the model is free of serial correlation and heteroscedasticity, whilst the CUSUM test indicates stability of the model coefficients.

The policy implication is for government to pursue policies that will enhance economic growth, through investment in growth enhancing sectors including agriculture, health, education, energy and infrastructure development; and ensure a politically stable environment as a recipe for private sector investment.

References

Addison, T., & Levin, J. (2012). The determinants of tax revenue in sub-Saharan Africa. Retrieved 21st August 2021 from http://www.diva-portal.org/smash/get/diva2:570456/FULLTEXT01.pdf

Adeleye, N. B. (2018). Time series analysis: Choosing optimal lags in Eviews. Retrieved September 8th, 2021, from http://cruncheconometrix.blogspot.com/2018/02/time-series-analysis-lecture-2-choosing.html

Aggrey, J., 2013. Determinants of tax revenue: Evidence from Ghana. Master’s Thesis, University of Cape Coast.

Agbeyegbe, T. D., Stotsky, J., & WoldeMariam, A. (2006). Trade liberalization, exchange rate changes, and tax revenue in Sub-Saharan Africa. Journal of Asian Economics, 17(2), 261-284. https://doi.org/10.1016/j.asieco.2005.09.003

AL-Qudah, A. M. (2021). The Determinants of Tax Revenues: Empirical Evidence From Jordan. International Journal of Financial Research, 12(3), Special Issue, 2021. https://doi.org/10.5430/ijfr.v12n3p43

Amoh, J. K., & Adom, P. K. (2017). The Determinants of Tax Revenue Growth of an Emerging Economy – the Case of Ghana. Int. J. Economics and Accounting, X(Y), 1-17. https://doi.org/10.1504/IJEA.2017.092280

Ansari, M. M. (1982). Determinants of tax ratio: A cross-country analysis. Economic and Political Weekly, 17(25), 1035-1042.

Ayenew, W. (2016). Determinants of tax revenue in Ethiopia (Johansen co-integration approach). International Journal of Business, Economics and Management, 3(6), 69-84. https://doi.org/10.18488/journal.62/2016.3.6/62.6.69.84

Bayu, T. (2015). Analysis of tax buoyancy and its determinants in Ethiopia (cointegration approach). Journal of Economics and Sustainable Development, 6(3).

Boukbech, R., Bousselhami, A., & Ezzahid, E. (2018). Determinants of tax revenues: Evidence from a sample of Lower Middle-Income countries. Applied Economics and Finance, 6(1), 11-20. https://doi.org/10.11114/aef.v6i1.3280

Castro, G. Á., & Camarillo, D. B. R. (2014). Determinants of tax revenue in OECD countries over the period 2001-2011. Contaduría y administración, 59(3), 35-59. https://doi.org/10.1016/S0186-1042(14)71265-3

Cung, N. H., & Son, T. T. (2020). Determinants of Corporate Income Tax Revenue in Vietnam. Advances in Management and Applied Economics, 10(1), 89-103.

Garg, S., Goyal, A., & Pal, R. (2014). Why Tax Effort Falls Short of Capacity in Indian States: A Stochastic Frontier Approach. Indira Gandhi Institute of Development Research (IGIDR), WP-2014-032.

Gupta, A. S. (2007). Determinants of tax revenue efforts in developing countries. IMF Working Papers, 2007(184). https://doi.org/10.5089/9781451867480.001

Gnangnon, S. K., & Brun, J. F. (2019). Trade openness, tax reform and tax revenue in developing countries. The World Economy, 42(12), 3515-3536. https://doi.org/10.1111/twec.12858

Gobachew, N., Debela, K. L., & Shibiru, W. (2018). Determinants of Tax Revenue in Ethiopia. Economics, 6(6), 58. https://doi.org/10.11648/j.eco.20170606.11

Gurdal, T., Aydin, M., & Inal, V. (2020). The Relationship between Tax Revenue, Government Expenditure, and Economic Growth in G7 Countries: New Evidence from time and Frequency Domain Approaches. Econ Change Restruct. https://doi.org/10.1007/s10644-020-09280-x

Jabari, R. (2020). Determinants of tax revenue mobilisation in Lesotho. (Thesis, University of Botswana).

Jafferi, A. A., Tabassum, F., & Asjed, R. (2015). An Empirical Investigation of the Relationship between Trade Liberalization and Tax Revenue in Pakistan. Pakistan Economic and Social Review, 53(2), 317-330.

Karagoz, K. (2013). Determinants of Tax Revenue: Does Sectorial Composition Matter. Journal of Finance, Accounting and Management, 4(2), 50-63.

Muibi, S. O., & Sinbo. O. O. (2013). Macroeconomic Determinants of Tax Revenue in Nigeria (1970-2011). World Applied Sciences Journal, 28(1), 27-35.

Neog, Y., & Gaur, A. K. (2020). Macro-economic determinants of tax revenue in India: an application of dynamic simultaneous equation model. International Journal of Economic Policy in Emerging Economies, 13(1), 13-35. https://doi.org/10.1504/IJEPEE.2020.106679

Nkoro, E., & Uko, A. K. (2016). Autoregressive Distributed Lag (ARDL) cointegration technique: application and interpretation. Journal of Statistical and Econometric methods, 5(4), 63-91.

OECD/ATAF/AU, (2020). “Revenue Statistics in Africa 2020”. Available on https://www.oecd.org/ctp/revenue-statistics-in-africa-2617653x.htm. Access on 29th October, 2021

Ojong, C. M., Anthony, O., & Arikpo, O. F. (2016). The impact of tax revenue on economic growth: Evidence from Nigeria. IOSR Journal of economics and finance, 7(1), 32-38.

Takumah, W., & Iyke, B. N. (2017). The links between economic growth and tax revenue in Ghana: an empirical investigation. International Journal of Sustainable Economy, 9(1), 34-55. https://doi.org/10.1504/IJSE.2017.080856

Terefe, K. D., & Teera, J. (2018). Determinants of tax revenue in East African countries: An application of multivariate panel data cointegration analysis. Journal of Economics and International Finance, 10(11), 134-155. https://doi.org/10.5897/JEIF2018.0924

UNCTAD (2010). Investment Policy Review of Sierra Leone. United Nations Conference on Trade and Development New York and Geneva: United Nations.

Wawire, N. (2017). Determinants of value added tax revenue in Kenya. Journal of Economics Library, 4(3) 322-344.

Wujung, V. A., & Aziseh, F. I. (2016). Assessing the effect of domestic resource mobilization on the economic growth of Cameroon. Aestimatio: The IEB International Journal of Finance, (12), 66-89. https://doi.org/10.5605/IEB.12.4

This work is licensed under a Creative Commons Attribution 4.0 International License.

Copyright for this article is retained by the author(s), with first publication rights granted to the journal.

This is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).